|

Claridge has been targeting the healthier segments of the food and beverage industry that are aligned with

positive demand trends and that will impact the industry medium to long term. As part of our industry analysis, we

regularly attend trade shows to get an overview of the trends shaping the North American industry. We are back from the Fancy Food Show and Expo West, where an impressive number of new products are launched every year. Amidst the noise, we seek to discern the trend-setting products from those that will exist for a short period of time. Identifying structural trends that will impact the sector longer term is a complex task, requiring a great deal of analysis and research, as well as extensive expertise in the sector. Forecasting food and beverage trends is very much a blend of both art and science given all the variables at play. We have made our best attempt at identifying the following seven trends that have caught our eye and are supported by demand signals. 1. Plant-Based Foods & Beverages Hit a Fever Pitch.  Over the last few years, plant-based foods and beverages have been one of the most prominent trends. Venture

capital firms have invested hundreds of millions of dollars in the category and the movement has found a

passionate community. Casual vegans/vegetarians and flexitarians are influencing the industry by representing a

growing proportion of the North American population. In fact, 14-20% of the adult population in the United States

is frequently or continuously following a vegan or vegetarian diet, while in Canada roughly 10% of the population

is said to be vegan or vegetarian. Casual vegans/vegetarians are people who consciously choose to limit their food

intake from animal sources (i.e., protein substitution) and/or increase their consumption of fruits and vegetables

(i.e., fruit and vegetables maximization). Whereas flexitarians primarily follow a vegetarian diet, but

occasionally eat meat or fish.

Over the last few years, plant-based foods and beverages have been one of the most prominent trends. Venture

capital firms have invested hundreds of millions of dollars in the category and the movement has found a

passionate community. Casual vegans/vegetarians and flexitarians are influencing the industry by representing a

growing proportion of the North American population. In fact, 14-20% of the adult population in the United States

is frequently or continuously following a vegan or vegetarian diet, while in Canada roughly 10% of the population

is said to be vegan or vegetarian. Casual vegans/vegetarians are people who consciously choose to limit their food

intake from animal sources (i.e., protein substitution) and/or increase their consumption of fruits and vegetables

(i.e., fruit and vegetables maximization). Whereas flexitarians primarily follow a vegetarian diet, but

occasionally eat meat or fish.This trend has impacted the way we incorporate vegetables in our diets. Affluent consumers in developed markets have embraced green juices made with kale and spinach, plant-based milks, vegetable/fruit chips and crackers, and spiralized vegetables (zucchini "spaghetti" instead of pasta) as they seek to eat more vegetables and minimize meat, sugar and wheat intake. Plants are increasingly replacing, without sacrificing enjoyment, meat and dairy products, therefore benefiting the environment and personal health. This trend touches a diversity of categories, as we are seeing frozen desserts made with dairy substitutes, and snacks. Also protein substitution is becoming more mainstream in other unexpected categories: seafood, jerky, ice cream and condiments. 2. Convenience: A Trend That's On-the-Go!  As the North American population adopts increasingly busier lifestyles, the importance consumers place on

minimizing food preparation has become paramount. Snack bars have evolved into meal replacements and consumers

look to eat 5+ small/quick meals per day, rather than the traditional three. In addition to snacking more

frequently, consumers are also looking for healthier indulgences within savory snacks.

As the North American population adopts increasingly busier lifestyles, the importance consumers place on

minimizing food preparation has become paramount. Snack bars have evolved into meal replacements and consumers

look to eat 5+ small/quick meals per day, rather than the traditional three. In addition to snacking more

frequently, consumers are also looking for healthier indulgences within savory snacks.In the past, consumers were forced to choose between either having a healthy meal or having a convenient meal. Now, consumers want both. Prepared salads, for example, have best captured this trend, as this category has seen tremendous growth in the last five years. Also, products that can offer high-protein content have grown in popularity, as consumers look for satiety in meal replacements. Significant innovations in soups going after the established brands, with better-for-you, portable, drinkable, and creative flavor offerings have contributed to a new category called "souping", representing a great quick meal. Souping is a new trend of consuming a blended soup as a chilled drink. Unlike juicing, souping retains some of the vegetable nutrients, mainly the fiber, that are usually squeezed out of a juice. Novel packaging alternatives have helped making consumers' lives easier in the last couple of years, simply by making products easier to open and/or to transport. 3. World Fusion: The Globalization of our Dishes.  Consumers are increasingly demanding bold, adventurous, and ethnic-inspired flavors and foods. Interest in

sampling the flavors of far-off lands opens the door to new opportunities. Demand for ethnic foods is following

the evolution in the U.S. population. In the 1990s, minorities represented roughly 25% of the population and the

proportion has increased to roughly 40% today . In North America, consumers are viewing ethnic foods as

"healthier" and more "flavorful" than traditional alternatives. Despite consumers increasingly wanting to

experiment with ethnic, spicy, and unique flavors, in many instances they are unsure how to create them. Pre-made

ethnic spice blends and sauces allow consumers to dip into new taste profiles, while still composing their own

meals. The growing interest in ethnic flavor foods is crossing over to beverages as well. They are now so

ubiquitous in our diet that consumers often forget the distant origin of some ingredients! Most people are

probably not aware that the recipe for Red Bull originates from Thailand.

Consumers are increasingly demanding bold, adventurous, and ethnic-inspired flavors and foods. Interest in

sampling the flavors of far-off lands opens the door to new opportunities. Demand for ethnic foods is following

the evolution in the U.S. population. In the 1990s, minorities represented roughly 25% of the population and the

proportion has increased to roughly 40% today . In North America, consumers are viewing ethnic foods as

"healthier" and more "flavorful" than traditional alternatives. Despite consumers increasingly wanting to

experiment with ethnic, spicy, and unique flavors, in many instances they are unsure how to create them. Pre-made

ethnic spice blends and sauces allow consumers to dip into new taste profiles, while still composing their own

meals. The growing interest in ethnic flavor foods is crossing over to beverages as well. They are now so

ubiquitous in our diet that consumers often forget the distant origin of some ingredients! Most people are

probably not aware that the recipe for Red Bull originates from Thailand.A good example of ethnic flavor is sriracha, which can now be found in almost every household and restaurant in North America. Matcha is also a great example. While it is mostly known for tea products, matcha is also used as a culinary ingredient (e.g., ice cream and chocolate bars, among others). Mochi is yet another example of a newer trend in dessert. Mochi is a Japanese delicacy that is created from sweet rice which is pounded into a paste. It can essentially be paired with almost everything, both culinary and confectionery. Finally, coconut is an example of a newer, ethnic ingredient in foods and beverages. The versatility of coconut is part of its appeal; it can be a single flavor product or be used in an array of combinations. 4. Next-Level Nostalgia.  Reinventing a stale category is not an obvious undertaking. However, some categories were recently upended by

creative brands who are now offering a sophisticated twist to some older categories, especially indulgence. While

consumers are still looking to indulge, they are also increasingly concerned with eating better; they want to eat

decadent foods without the guilt, and/or they seek new twists to their favorite childhood treats.

Reinventing a stale category is not an obvious undertaking. However, some categories were recently upended by

creative brands who are now offering a sophisticated twist to some older categories, especially indulgence. While

consumers are still looking to indulge, they are also increasingly concerned with eating better; they want to eat

decadent foods without the guilt, and/or they seek new twists to their favorite childhood treats.In the better-for-you indulgence category, examples range from making healthier candy and snack options (UNREAL Candy, Brookside) to a company making banana-based non-dairy frozen desserts (Hakuna Banana). In the "new twist" category, examples range from upscale, unexpected flavored cotton candy (Sugar and Spun) and marshmallow (Smashmallow) to being able to eat cookie dough without any worries, just like ice cream and with some vegan options (Edoughble). 5. With Beverages Overflowing: Three Stars Stand Out in the Category.  Carbonated soft drinks, once the most consumed beverages in North America, have been declining for several years.

Health preferences, increased regulation and innovative technology are spurring beverage manufacturers to

introduce new products to the market. Over the last few years, the category has seen a lot of innovation,

especially among functional beverages. Functional beverages are typically intended to convey a health benefit. In

our opinion, three functional beverages are poised to set long term trends in the market: kombucha, clean energy

drinks, and cold brew coffee.

Carbonated soft drinks, once the most consumed beverages in North America, have been declining for several years.

Health preferences, increased regulation and innovative technology are spurring beverage manufacturers to

introduce new products to the market. Over the last few years, the category has seen a lot of innovation,

especially among functional beverages. Functional beverages are typically intended to convey a health benefit. In

our opinion, three functional beverages are poised to set long term trends in the market: kombucha, clean energy

drinks, and cold brew coffee.Kombucha is a tea-based fermented drink believed to be beneficial for digestive issues and gut health. Ready-to- drink teas are gaining market share against carbonated soft drinks, as consumers are becoming attuned to the health risks posed by excessive sugar consumption. At 30 calories per cup of pure kombucha, where no fruit juice or puree is added, it is a better choice than drinking sodas, which can contain more than 90 calories per cup. Clean energy drinks are among the beverages that have the fastest growth rate. These drinks are made of natural stimulants, like guarana and guayusa, providing longer lasting energy over caffeine. Unlike typical caffeinated energy drinks, they usually contain less sugar. In addition, many are being certified organic or even GMO-free. Cold brew coffee is one of the fastest growing categories in North America. Cold brewing is a method that involves soaking coffee grounds in water without using heat. The resulting coffee is less acidic, smoother in taste than other brewing methods, and tends to be highly caffeinated. As a result, it is easier on people with sensitive stomachs. The natural sweetness of cold brew eliminates the need for large amounts of sugar or milk, resulting in a caffeinated beverage low in sugar. This gives it an advantage over regular energy drinks and carbonates, which are what consumers usually buy if they need an energy boost. 6. Mini Portions: A Trend That Stands Tall.  Small bite size treats and snacks are quickly moving to bite size pieces (chocolate, candy, jerky, bars, etc.),

where you can take in your hand and pop into your mouth. These smaller portions are popular, especially in sweet

snacking, where they offer a chance to capture the impulse indulgence buyer. As snacking has gained in popularity,

they also provide to consumers an opportunity for greater portion control. Controlling portion sizing remains the

primary step to proper eating habits. A great example is from Kasugai, a popular Japanese snack company, which

makes individually wrapped fruit gummy candies.

Small bite size treats and snacks are quickly moving to bite size pieces (chocolate, candy, jerky, bars, etc.),

where you can take in your hand and pop into your mouth. These smaller portions are popular, especially in sweet

snacking, where they offer a chance to capture the impulse indulgence buyer. As snacking has gained in popularity,

they also provide to consumers an opportunity for greater portion control. Controlling portion sizing remains the

primary step to proper eating habits. A great example is from Kasugai, a popular Japanese snack company, which

makes individually wrapped fruit gummy candies. 7. Mini Portions: A Trend That Stands Tall.  Consumer demand for healthier and more natural products containing no artificial ingredients continues to grow,

with artificial sweeteners losing favor among health-conscious shoppers and refined sugar consumption declining.

Growing health consciousness has resulted in consumers being increasingly cautious of artificial ingredients, such

as colorants and flavorings. In this environment, interest has exploded in utilizing honey, dates and maple syrup

as natural sweetener replacements in coffees, teas, snack bars, hot cereals, and in home-cooked meals.

Consumer demand for healthier and more natural products containing no artificial ingredients continues to grow,

with artificial sweeteners losing favor among health-conscious shoppers and refined sugar consumption declining.

Growing health consciousness has resulted in consumers being increasingly cautious of artificial ingredients, such

as colorants and flavorings. In this environment, interest has exploded in utilizing honey, dates and maple syrup

as natural sweetener replacements in coffees, teas, snack bars, hot cereals, and in home-cooked meals.For many consumers, honey is an instantly recognizable natural sweetener, and its unique taste and texture make it a highly versatile sweetening agent that has more positive connotations as large portions of consumers attempt to cut back on sugar consumption. Furthermore, honey has been known for years as having antibacterial properties. Now, propolis, the "glue" that keeps everything together in the beehive, is said to have additional benefits for humans. However, dates seem to be standing out amongst alternative sweeteners, as they are a nutritious and lower-glycemic substitute for sugar and honey. They are frequently used in baking, as they sweeten and help ingredients stick together. Key Takeaways Claridge is targeting companies that are supported by the previously mentioned structural trends shaping the industry. We seek companies that have at least one of the following characteristics: convenience, ethnic, healthy and sustainable, and indulgence, with science and IP at the core of their strategy. In an increasingly crowded market, having a differentiated story and great direct-to-consumer capabilities are key enablers.

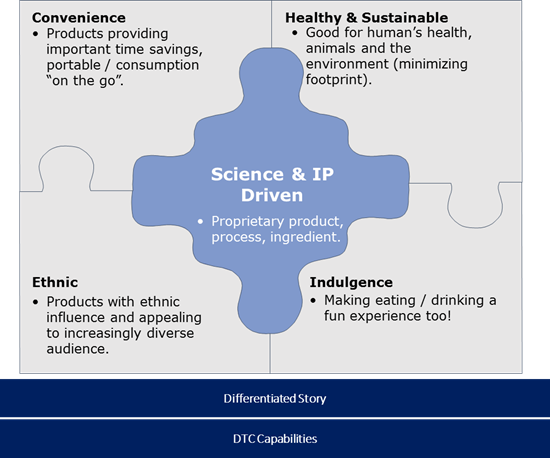

|